There’s a lot of restaurant tech these days. The average restaurant uses at least 15 major software tools to run their business—from accounting and scheduling to payroll and loyalty. This year we are seeing the results of 10+ years of hospitality tech innovation from three industry staples: Doordash, Olo and Toast. Doordash recently went public and soon after Olo and Toast announced their plans to get listed.

Each of these companies represents one of the three main pillars of restaurant tech: marketplace (Doordash), middleware (Olo), and point-of-sale (Toast). Here are my insights about what made these three acclaimed tech businesses ready for the public markets.

The Doordash Insight: Everyone wants to outsource logistics

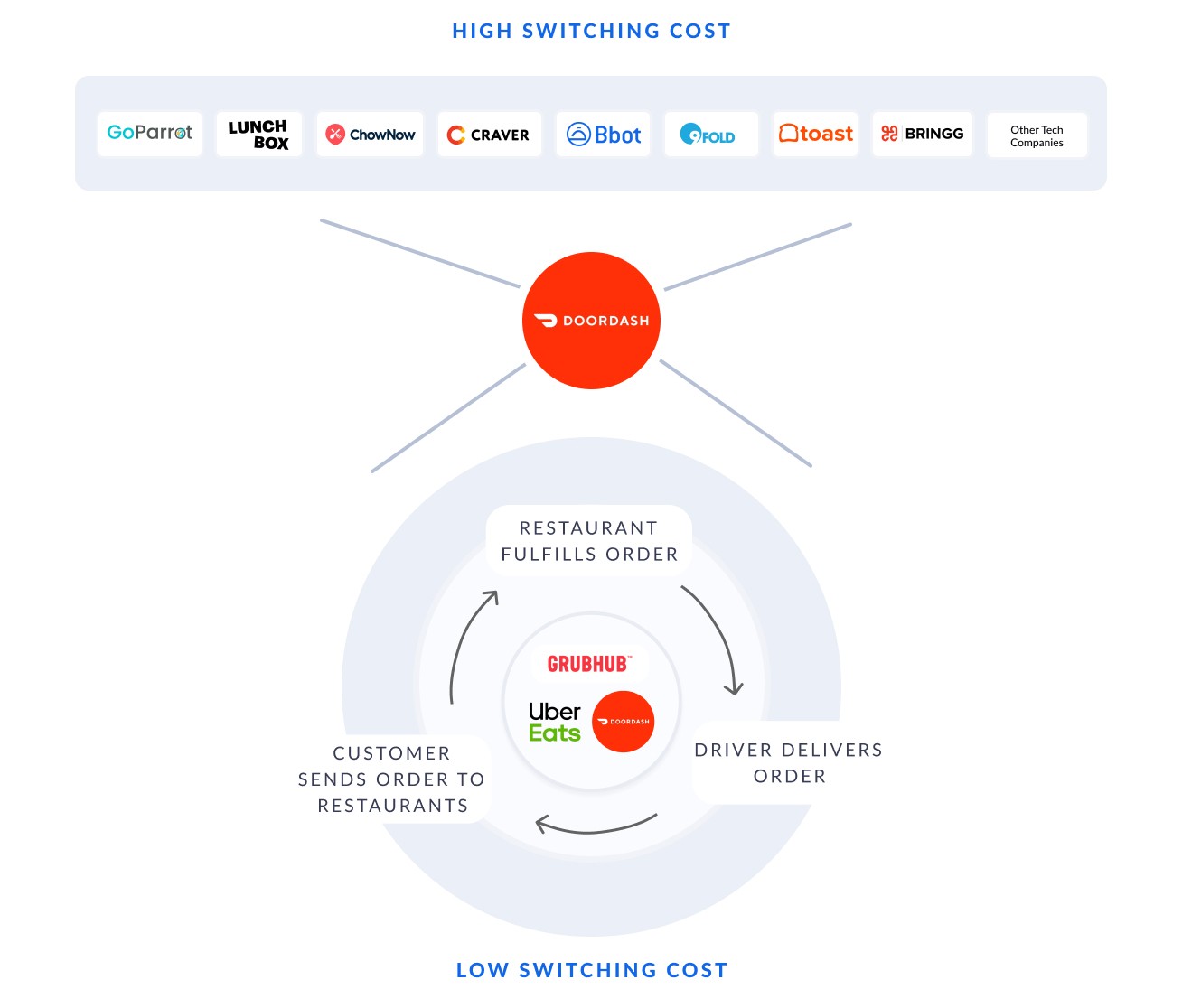

If you’ve read any of my posts on LinkedIn, you probably know I am fascinated by Doordash’s journey (disclaimer: I own some of the company’s stock). During a period of intense competition with Seamless, Postmates, Uber and GrubHub, Doordash has somehow come out incredibly strong (they maintain 55% market share, more than the others combined). It’s because they have something different to offer.

Doordash no longer just serves as a marketplace where consumers can browse, order and get delivery from their favorite neighborhood spots. They have unbundled their driver network and the logistics of food delivery; today, all kinds of tech companies (and restaurants who build their own custom platforms) can leverage Doordash’s driver network via their application interface (API).

Their insight? More—much more—restaurant tech is coming and most entrepreneurs don’t want to build a full logistics network. Frankly, it’s just too easy to integrate with a company like Doordash that is in every city across the country and has hundreds of thousands of drivers at the ready.

For delivery, Doordash will continue to make more profit per order than those tech companies, like Chownow, that write the UIs.

The Olo Insight: Enterprise customers demand a custom UI and their own credit card processing

In Olo’s S-1, they acknowledge that their current offerings are focused on enterprise restaurants, of which there are approximately 300,000 individual units across the U.S. Since 2005, Olo has been creating middleware—software that the average consumer never sees or touches—but is used by brands like Chili’s, Applebees and Cheesecake Factory. Their software allows the enterprise restaurant to build or maintain their own user interface (e.g., their own custom website and app) and still connect all kinds of third-party ordering and loyalty services. Olo provides the pipes that send the orders from all over the web.

Over the years, Olo has built a huge moat. That moat is not based on their restaurant tech; it’s based on a deep understanding of the fact that their enterprise customer does not want an out-of-the-box anything. The enterprise wants to work with their own creative team to develop a custom experience, and they want to preserve their relationships with their design agencies and credit card processing companies—while also remaining nimble enough to work with newcomers to hospitality such as marketplaces, loyalty providers, and social media apps. Olo promises enterprise restaurants can keep what they have, and keep adding so they are ready for “whatever is coming next” (that quote is from their website homepage).

One last insight from Olo’s S-1: while their revenue model used to be based primarily on a monthly subscription cost, they are now telling investors that they are looking at or implementing “per order” monetization schemes.

The Toast Insight: The majority of real-world transactions happen inside of small business restaurants (not enterprise)

Every industry has been adapting to cloud-based computing and the restaurant industry is no different. Toast was the company to really get traction by offering everything a small restaurant would need: a durable, Android-based hardware product with a lower startup cost. They delayed their own revenue, but made it back over time by charging their customers slightly higher processing fees—aligning incentives with restaurant success.

When Toast’s S-1 comes out it will list a much larger addressable market than Olo. Instead of 300,000, Toast has focused on the 700,000 small business restaurant locations across the U.S., based on 2019 NPD Group data. Their go-to-market strategy makes sense here too; while pursuing enterprise seems efficient (and it does make sense for Olo), it can be just as rewarding to target SMB because, at a unit level, many SMBs do much higher sales than any individual enterprise unit. With a smart and targeted go-to-market team, Toast has shown that there’s a huge opportunity in hospitality SMB.

It can be just as rewarding to target SMB because, at a unit level, many SMBs do much higher sales than any individual enterprise unit.

Oh yeah, and hardware is super sticky and once they are in-venue no one wants to take them out.

But wait for it…

My Prediction: Online ordering for restaurants and website presence will overtake POS hardware as the first solution hospitality companies select

For the last 40 years, whenever a new restaurant has opened, the first restaurant technologies they decide on is their hardware point-of-sale. Everything else they layer in had to be built around this platform.

But today restaurants must adapt to the fact that digitally-native guests want to interact and engage with them in the medium that they prefer: Instagram, Whatsapp, Goldbelly, Slice, Seated, Snackpass and so on. No longer is the point-of-sale just a piece of hardware in the corner of the bar, it has evolved to be everywhere the guest wants to be.

As Doordash, Olo, and Toast pivot to focus on scale and delivering for their shareholders, the next generation of restaurant technologies will rise up and continue to deliver on innovation that the market continues to demand.